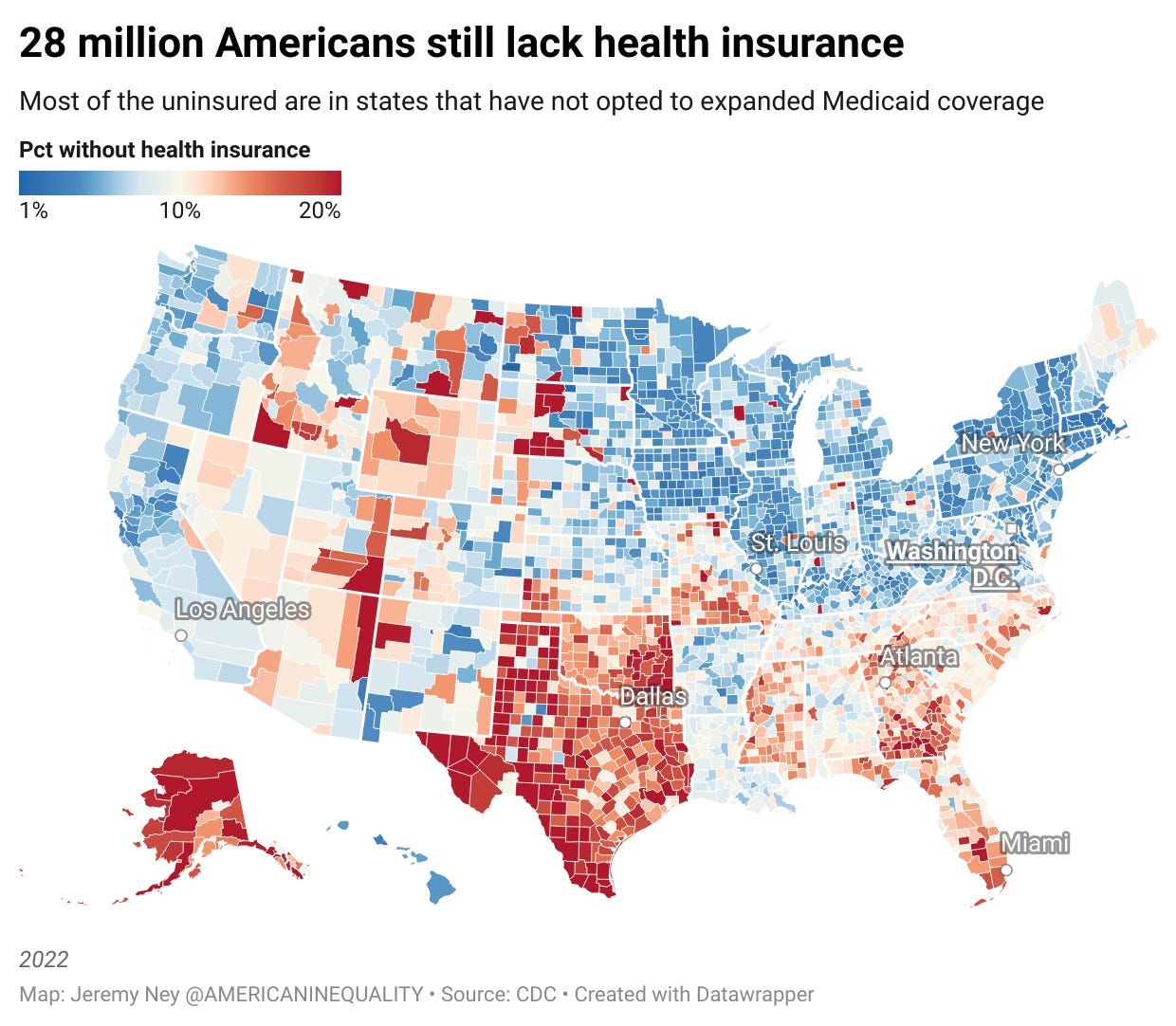

Without health insurance, poverty is just a medical bill away

Remember the Affordable Care Act? We still have a long way to go

American Inequality has now hit +7,000 email subscribers! 🎉 Send to a friend and tell them to join our rapidly growing community 🚀

INTERESTING ON THE WEB

Great free class from On Data & Design on how to map out data - YouTube

Visualizing how Colorado River water gets used up (spoiler alert: the data viz is a river) - The New York Times

America is the only